Lihat juga

30.03.2026 12:33 PM

30.03.2026 12:33 PMTensions in the Middle East sharply intensified at the end of last week after President Trump, at a March 26 press conference, proposed seizing Iran's Kharg Island, through which 90% of Iran's oil exports pass, which could mean a shift from stand-off strikes to direct combat aimed at gaining control of resources.

Market reaction, however, remains rather restrained. Yes, oil rose, but not critically, and has not yet reached the 2008 highs; equity indices reacted weakly, and profit forecasts remain resilient. All of this still needs to be re-priced, and only then will strong movements begin.

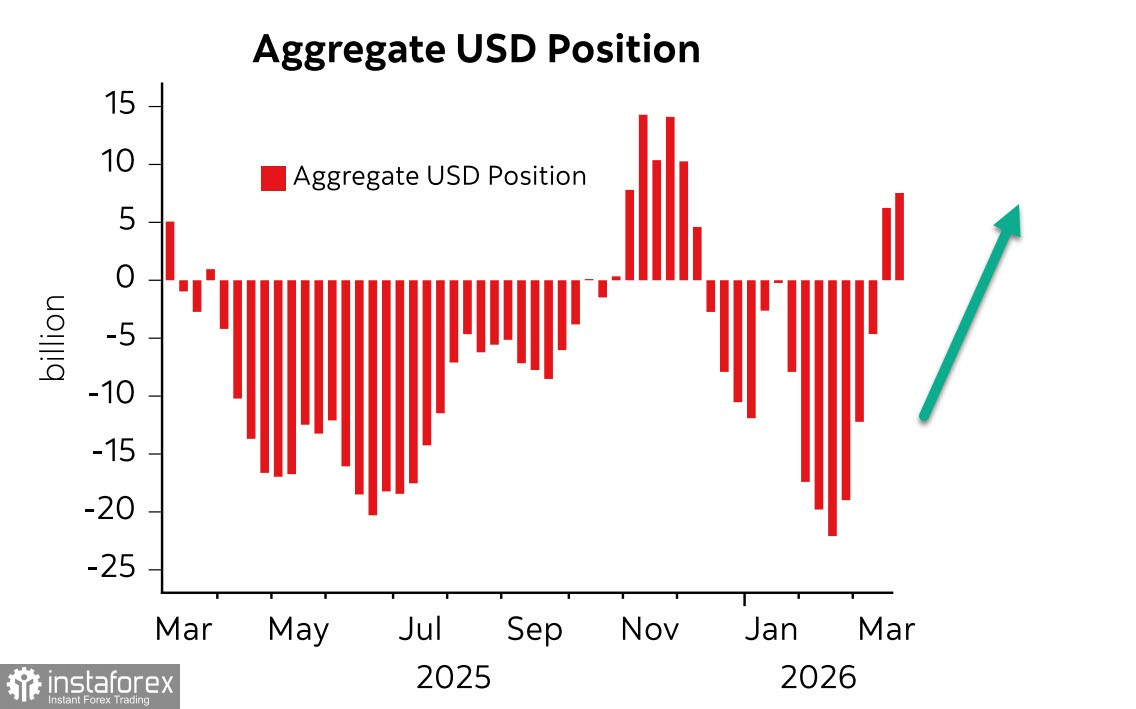

The aggregate long position in the US dollar increased by $1.2 billion over the reporting week to $7.4 billion, an increase that is relatively small compared with the prior three weeks, but still an increase. It is unclear how the gamble in the Persian Gulf will affect the US economy itself, how other countries will respond, and whether the reverse effect will occur, with the US provoking accelerated de-dollarization instead of securing energy control. For now, everything is uncertain; we will rely on specific data, specific news, and changes in currency flow directions.

As for economic news, the main data will arrive toward the end of the week. ISM indices for March, the ADP private payrolls report, Challenger job cuts, the trade balance, nonfarm payrolls, and a number of secondary indicators will be published. They may show an unattractive picture of slowing growth together with rising inflation, that is, stagflation in aggregate.

The Michigan consumer survey released on Friday showed a sharp drop in consumer sentiment and, simultaneously, a rise in one-year inflation expectations, which overall confirms the stagflation threat. Consumer moods are not merely pessimistic but comparable to the worst economic periods.

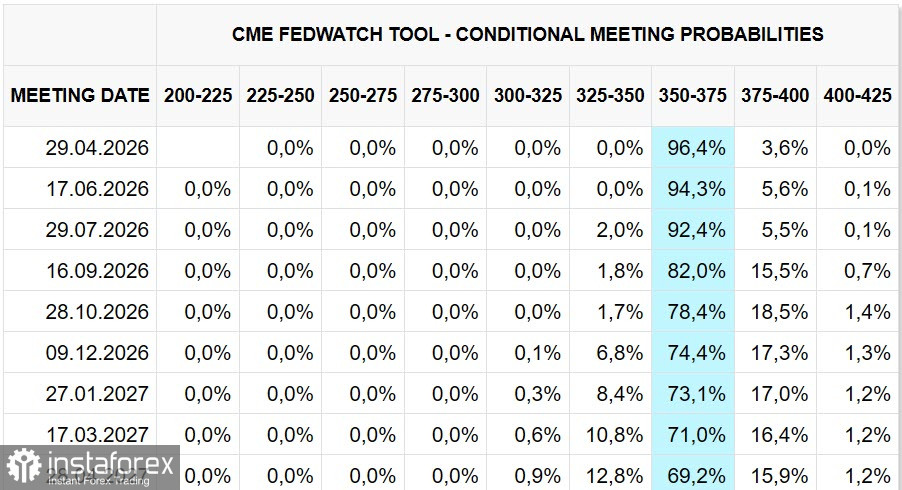

Fed funds futures imply the current rate will be held through the end of 2027; there is no movement in this outlook yet.

Bond yields have been rising for the past month, and Monday opened with another rise. For the US, where 10-year Treasuries have approached 4.5%, this is a big problem — the rapid growth of public debt together with rising yields sharply increases the budgetary burden, and the budget is already deeply in deficit. The situation must be resolved in an acceptable way in the coming months; otherwise, the US will accelerate toward default.

Investors assume that the current rise in oil prices is only the first stage of a protracted energy crisis. The US stock market on Friday suffered its largest drop since January due to fears of further escalation; the S&P 500 fell to its lowest level since September 2025.

For now, however, we proceed from the obvious — the current situation favors further strengthening of the dollar.