یہ بھی دیکھیں

12.02.2026 09:23 AM

12.02.2026 09:23 AMYesterday, equity indices closed mixed. The S&P 500 declined by 0.01%, while the Nasdaq 100 fell by 0.16%. The Dow Jones Industrial Average also slipped by 0.13%.

However, Asian indices continued to rise for the fifth consecutive day, widening their lead over the American ones this year as relatively lower valuations and firmer growth prospects attracted buyers. The MSCI Asia Pacific index rose by 0.6%, reaching a record high. Since the start of the year, the index has gained roughly 13%, delivering the best start to the year compared with the S&P 500. The American index added just 1.4%, ranking 69th out of 92 indices. South Korea was the best-performing market in the world, up 30%.

Treasury yields continued to decline, falling to 4.18%, as traders revised expectations for Federal Reserve rate cuts this year. Money markets have already priced in the next Fed rate cut only for July, whereas previously a June cut had been expected. This followed the release of the jobs report showing that the US economy added 130,000 new jobs in January, twice the forecast.

Such a substantial employment surge, exceeding even the most optimistic expectations, prompted the market to reassess the probability of imminent monetary easing by the Federal Reserve. Previous market expectations had assumed that the Fed would likely begin a cycle of rate cuts as early as June in response to signs of a potential labor market slowdown. However, January's data demonstrated surprising resilience and strength in the US economy. The creation of 130,000 jobs, more than double the forecast 60,000–70,000, indicates the economy continues to show solid growth despite slowdown concerns. This forced money market participants to adjust their forecasts, pushing the expected first rate cut to July.

With a strong labor market and no clear signs of a recession, the central bank is likely to prefer keeping current interest rates higher for longer to avoid reigniting inflation. This means any further rate cuts will depend on new, more convincing signals of weakness in economic activity or disinflationary pressure.

In other market segments, Bitcoin fell to trade around $67,100, while the Dollar Spot Index recovered earlier losses and rose by 0.1%. Ultra-long-term Japanese bonds continued their post-election rally as the historic victory of Prime Minister Sanae Takaichi eased investor concerns over fiscal policy. Oil prices gained as tensions in the Middle East outweighed concerns about a growing supply glut. Gold declined after strong US labor market data reduced expectations of a Fed rate cut.

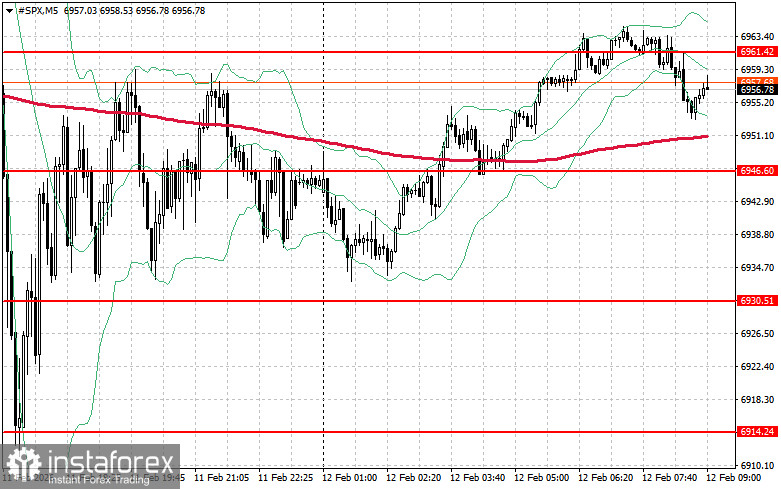

As for the technical picture of the S&P 500, the primary task for buyers today will be to overcome the nearest resistance level of $6,961. This would help the index gain upside momentum and open the possibility of a push to a new level at $6,975. Equally important for bulls will be maintaining control above $6,989, which would strengthen buyers' positions. In the event of a downside move amid weakening risk appetite, buyers will need to reassert themselves around $6,946. A break below that level would quickly push the instrument back to $6,930 and open the path to $6,914.