19.05.2026 08:51 AM

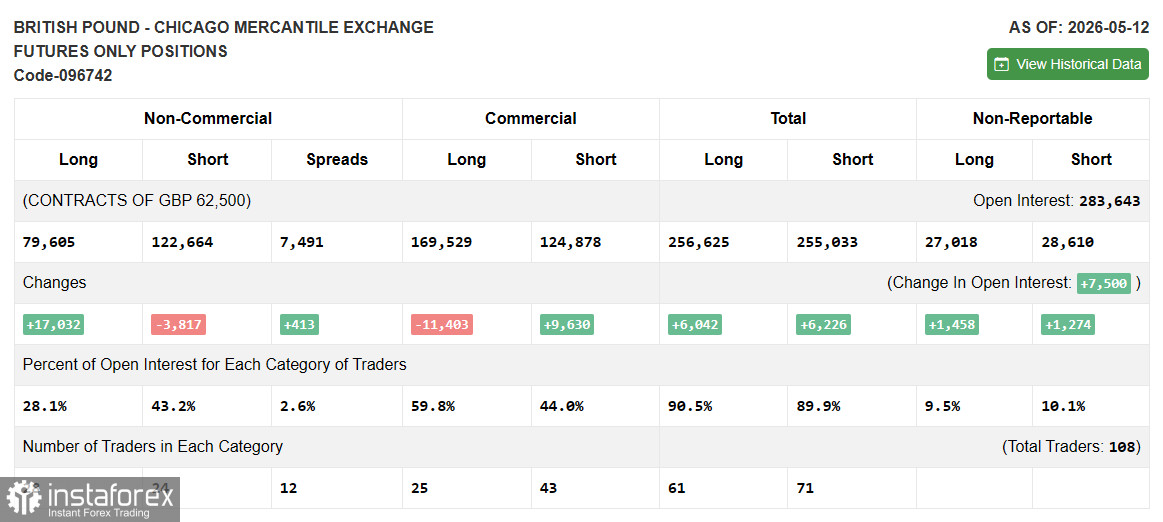

19.05.2026 08:51 AMThe structure of the COT report for the pound presents a contradictory but overall bearish picture.

Open Interest (OI): 283,643 contracts (each contract is £62,500). Increased by +7,500 over the week.

Long: 79,605 (28.1% of OI) — increased by +17,032

Short: 122,664 (43.2% of OI) — decreased by -3,817

Spreads: 7,491 (2.6% of OI) — increased by +413

Speculators have sharply reduced their shorts and aggressively increased their longs; however, the net position remains bearish, with shorts still significantly greater (43.2% vs. 28.1%). Number of traders: 28 long / 24 short.

Long: 169,529 (59.8% of OI) — decreased by -11,403

Short: 124,878 (44.0% of OI) — increased by +9,630

Hedgers have sharply shifted towards selling this week: they have reduced their longs and increased their shorts, which itself is a bearish signal. Nevertheless, their net position remains long (59.8% vs. 44.0%). Number of traders: 25 long / 43 short.

Long: 256,625 (90.5% of OI)

Short: 255,033 (89.9% of OI)

Total positions are practically balanced — the market is in a state of uncertainty.

Long: 27,018 (9.5% of OI) — increased by +1,458

Short: 28,610 (10.1% of OI) — increased by +1,274

Small traders are nearly neutral — longs and shorts are almost equal.

As noted above, the structure of the COT report for the pound paints a contradictory but generally bearish picture. Despite the aggressive covering of shorts by speculators (+17,032 longs over the week) — which itself seems like a bullish movement, their net position remains deeply negative: shorts (43.2%) still significantly exceed longs (28.1%). An even more concerning signal is the behavior of hedgers: they have sharply reduced their longs (-11,403) and increased their shorts (+9,630) — a shift that professional market participants use to hedge against the weakening of the pound. The total open interest has risen by +7,500 contracts, but the increase is mainly in short positions among commercial players, intensifying pressure on GBP/USD.

All of this is heavily influenced by the conflict in the Middle East, which has become a global event in energy security, leading to disruptions in shipping, reduced LNG availability, and rising risk premiums on energy commodities. The UK, as a major importer of energy resources, is particularly vulnerable to such shocks: rising gas and oil prices directly affect inflation and consumer demand within the country. Thus, a prolonged war in the Middle East could provoke a larger and more sustained increase in energy prices than expected, adding to inflationary pressures. For the Bank of England, this means the same dilemma faced by the European Central Bank— but with the consideration that the British economy is historically more sensitive to energy shocks. In a situation where major players are clearly hedging against the risk of a weakening pound and geopolitical tensions persist, the COT data indicate the market is not in a hurry to bet on a sustainable rise in GBP/USD.