Lihat juga

26.02.2026 02:53 PM

26.02.2026 02:53 PM

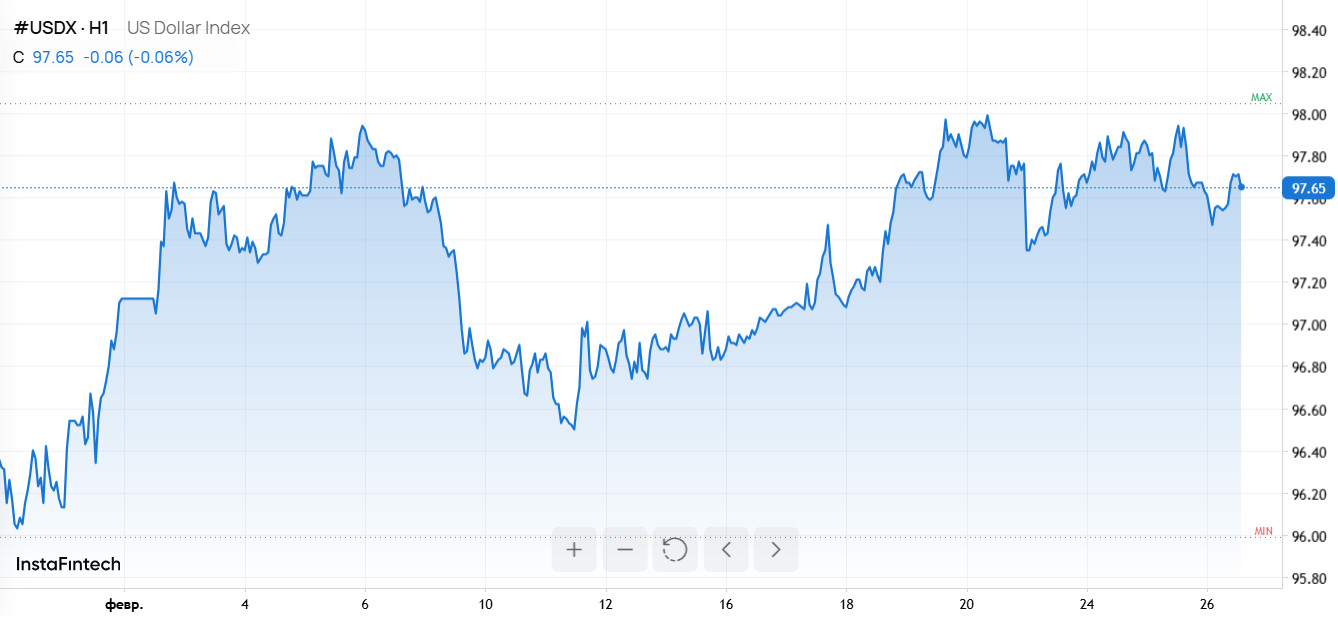

The US dollar recovered on Thursday after early losses following strong results from tech giant Nvidia, while traders prepared for details of the new tariff policy and monitored diplomatic talks. The dollar index remains on track for a small weekly decline but continues to show volatility driven by corporate earnings and geopolitics.

At 11:00 (08:00 GMT), the dollar index, which tracks the US currency against a basket of six other currencies, was up 0.1% at 97.650, though it is down about 0.2% for the week.

The dollar's early drop was the market's reaction to Nvidia's report: the company's sales for the January quarter beat analysts' expectations and its revenue guidance for the current quarter topped forecasts, boosting risk appetite and reducing demand for the safe?haven currency.

ING analysts note, "Improved sentiment has put pressure on the dollar over the past 24 hours, with only the yen suffering a larger defeat among G10 currencies yesterday."

Traders are nevertheless watching closely for any reaction from the US administration to the Supreme Court's February 20 ruling that struck down the president's emergency tariffs. On Wednesday, US Trade Representative Jamison Greer said tariff rates for some countries would rise to 15% or higher from the recently introduced 10%, without naming specific trading partners or providing further details.

Another source of uncertainty is meetings between US and Iranian officials in Geneva to discuss a nuclear deal. US President Donald Trump warned that "bad things" could happen to the Middle Eastern country if meaningful progress is not achieved.

ING argues that "any escalation there looks like the most probable catalyst for a broader dollar rally, given the confidence from Nvidia's results and a lack of major data releases."

Still, the bank adds, "Overall, we may see some dollar stabilisation today, although some downside risks remain since the positive effect from Nvidia's results could keep markets away from safe?haven currencies a little longer."

FX moves and data

EUR/USD fell 0.1% to 1.1798; consumer confidence data for the euro area are due during the session. However, both that report and Friday's inflation numbers are unlikely to move the euro much — the ECB is expected to keep rates unchanged.

"For now, the short-term interest rate differential for EUR: USD remains unfavourable for EUR/USD, but we have not seen a sufficient restoration of confidence in the dollar to forecast a major decline from here. We still view 1.1750 as solid support, barring a serious escalation in Iran," ING says.

GBP/USD dropped 0.3% to 1.3523. The pound has struggled to respond to improved sentiment in the UK business and professional services sector: the quarterly CBI survey showed optimism rising to -3 in February from -50 in November, the highest reading since August 2024, but this has yet to translate into strong gains for sterling.

In Asia, USD/JPY fell 0.3% to 156.01 after Bank of Japan governor Kazuo Ueda told the Yomiuri Shimbun that policymakers will study incoming data at the March and April meetings, leaving open the possibility of another rate increase if inflation and wage trends remain firm. Those comments heightened expectations for a gradual normalisation of monetary policy in Japan. Earlier, the yen had weakened after reports that Prime Minister Sanae Takaichi voiced caution about further rate hikes, following the nomination of two dovish candidates to the BOJ board.

On the mainland, USD/CNY sank 0.4% to 6.8392, sliding to a fresh 34-month low amid expectations of policy support ahead of China's annual parliamentary session, the National People's Congress. Investors expect growth targets and potential fiscal stimulus signals that will set Beijing's priorities this year.

Other crosses: AUD/USD slipped 0.1% to 0.7114, NZD/USD fell 0.2% to 0.5988.

How traders can profit from the situation

Keep an eye on the economic calendar (euro area consumer confidence, inflation prints, and central bank meetings) and news on tariffs — today's FX direction is being set by a mix of corporate reports, policy decisions and geopolitics.