یہ بھی دیکھیں

20.05.2026 12:40 PM

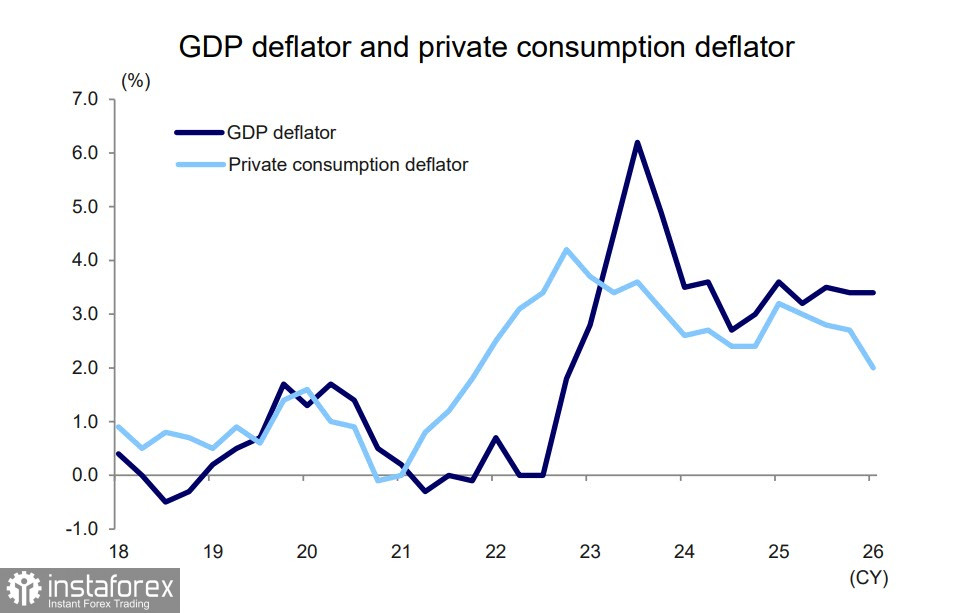

20.05.2026 12:40 PMThe first preliminary estimates of Japan's GDP for the first quarter of 2026, published on May 19, indicate real growth of +0.5% quarter-on-quarter (or +2.1% year-on-year). Thus, the economy has expanded for a second consecutive quarter.

Growth was driven less by domestic demand and more by external demand. Real household incomes increased by 1.3%, and, at least as of the first quarter, the Japanese economy appeared relatively resilient.

Bank of Japan Governor Kazuo Ueda commented on the GDP data, noting that they generally matched expectations. Nevertheless, he acknowledged that the pass-through of price pressures from the initial stages of the production chain to intermediate stages is occurring somewhat faster than usual. He also stated that he and his team would closely monitor the results of the Tankan business sentiment survey, as well as inflation expectations reflected in the market for inflation-indexed government bonds. It appears that the Bank of Japan is beginning to worry about future price growth.

The consequences of the Persian Gulf conflict are already beginning to affect Japan's economy and finances. The ratio of profits to losses has moved even deeper into negative territory. It is evident that import deflator growth has outpaced export deflator growth due to the weakening yen and the sharp rise in energy prices. Terms of trade deteriorated for the second consecutive month in April, and there is no reason to expect improvement.

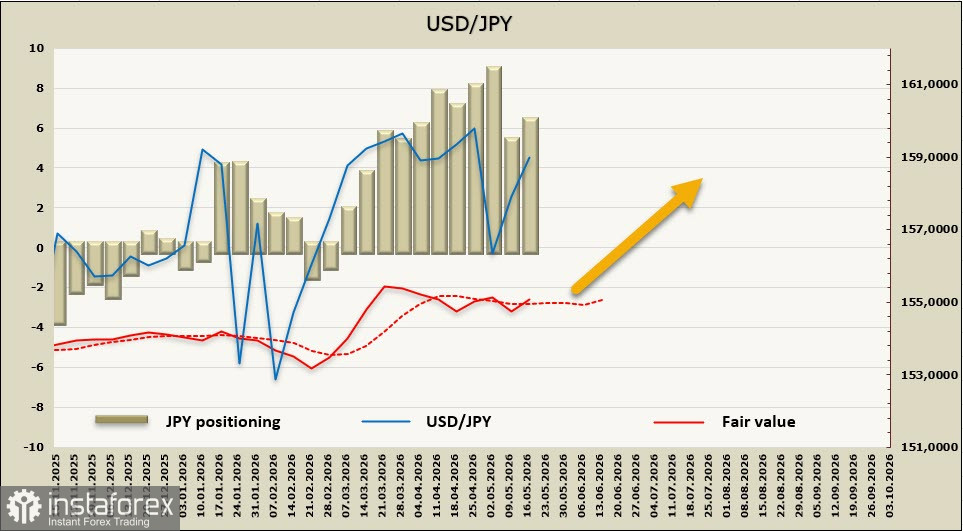

Pressure on public finances is increasing. In March, Japan reduced its holdings of U.S. Treasury bonds by $47 billion. It is quite possible that these funds were used during a currency intervention, as the government lacks free reserves for such measures.

If the yen continues to weaken, another intervention may be required. Under IMF rules, Japan may take such a step only once before November in order to avoid putting the yen's status as a market currency at risk. Accordingly, any movement in USD/JPY toward the 162 level would be viewed not merely as undesirable weakening, but perhaps as an existential threat carrying risks for the stability of the entire system.

If intervention becomes impossible, the only remaining option for Japan's financial authorities would be a Bank of Japan rate hike aimed at increasing yields and, consequently, the attractiveness of the yen. Each rate increase creates additional pressure on the budget due to Japan's extremely large public debt, making debt servicing more expensive. Nevertheless, such a move would allow the Ministry of Finance to buy time while waiting for the Gulf conflict to end and supply chains to stabilize.

Perhaps the rising probability of a June rate hike will cool bearish sentiment toward the yen and make more radical measures unnecessary. However, if the escalation period drags on, Japan may face difficult times.

The net short position on the yen increased by $1.1 billion during the reporting week to $6.0 billion. Speculative positioning remains firmly bearish, while the estimated fair value continues to fluctuate near the long-term average without a clear direction.

A week earlier, we assumed that the growing likelihood of a Bank of Japan rate hike would help strengthen the yen. However, investors apparently are not concerned about the possibility of another intervention, and the yen continues to weaken, once again approaching the strategic level of 162. The probability of a pullback toward support at 155.90/156.20 has decreased.

In the current situation, only a rapid de-escalation of the conflict and the reopening of the Strait of Hormuz could support the yen, but for now such an outcome appears unlikely.