আরও দেখুন

10.03.2026 12:40 AM

10.03.2026 12:40 AMThe rise in oil prices above $110 per barrel has dealt a devastating blow to the euro. As noted by ANZ, EUR/USD traditionally reacts sensitively to shocks in the oil market. Four years ago, due to the armed conflict in Ukraine, the regional currency fell below parity. This was related to the displacement of the largest producer, which had an output of about 10 million barrels per day. Now, the focus is on the disruption of the main Brent route from the Middle East to Europe and Asia, which, according to JP Morgan, could result in a global supply deficit of 10 million barrels per day.

The Eurozone is a net importer of energy products, and the sharp rise in oil and gas prices could leave its economy vulnerable. It's no surprise that weekly reversal risks for the euro have fallen to their lowest levels since the COVID-19 pandemic and the U.S. and French presidential elections, which were marked by spikes in geopolitical tension. Today, that tension is reaching unprecedented heights.

The conflict in the Middle East has changed sentiments in the futures market across different time frames. Previously, the current decline in EUR/USD was considered merely a correction to the upward trend, but the beginning of spring has completely reversed that outlook. Annual reversal risks for the euro have dropped to their lowest level since Friedrich Merz shocked Europe with fiscal stimulus. Has the bullish trend for the primary currency pair reversed?

Bad news does not come alone. Led by Chancellor Merkel, the Christian Democratic Union lost local elections in Baden-Wurttemberg, despite polls showing the ruling party's advantage over the victorious Greens. This development has only added fuel to the EUR/USD decline.

However, the main reason for the euro's fall is the looming threat of stagflation over the global economy. If oil prices indeed rise to $150 per barrel, as Qatar predicts, inflation will surge, while global GDP will sharply slow. In such a scenario, global risk appetite will fall, dragging down U.S. stock indices.

Yardeni has raised the probability of sharp sell-offs in the U.S. stock market for the remainder of the year from 20% to 35%. A decline in the S&P 500 and Nasdaq Composite will strengthen demand for safe-haven assets. The primary safe-haven asset in the context of the armed conflict in the Middle East is the U.S. dollar.

The euro receives no assistance from increased expectations of an ECB deposit rate hike. The futures market believes in at least one act of monetary expansion in 2026. It's unlikely that the central bank will tighten monetary policy amid the energy crisis. That would be too risky.

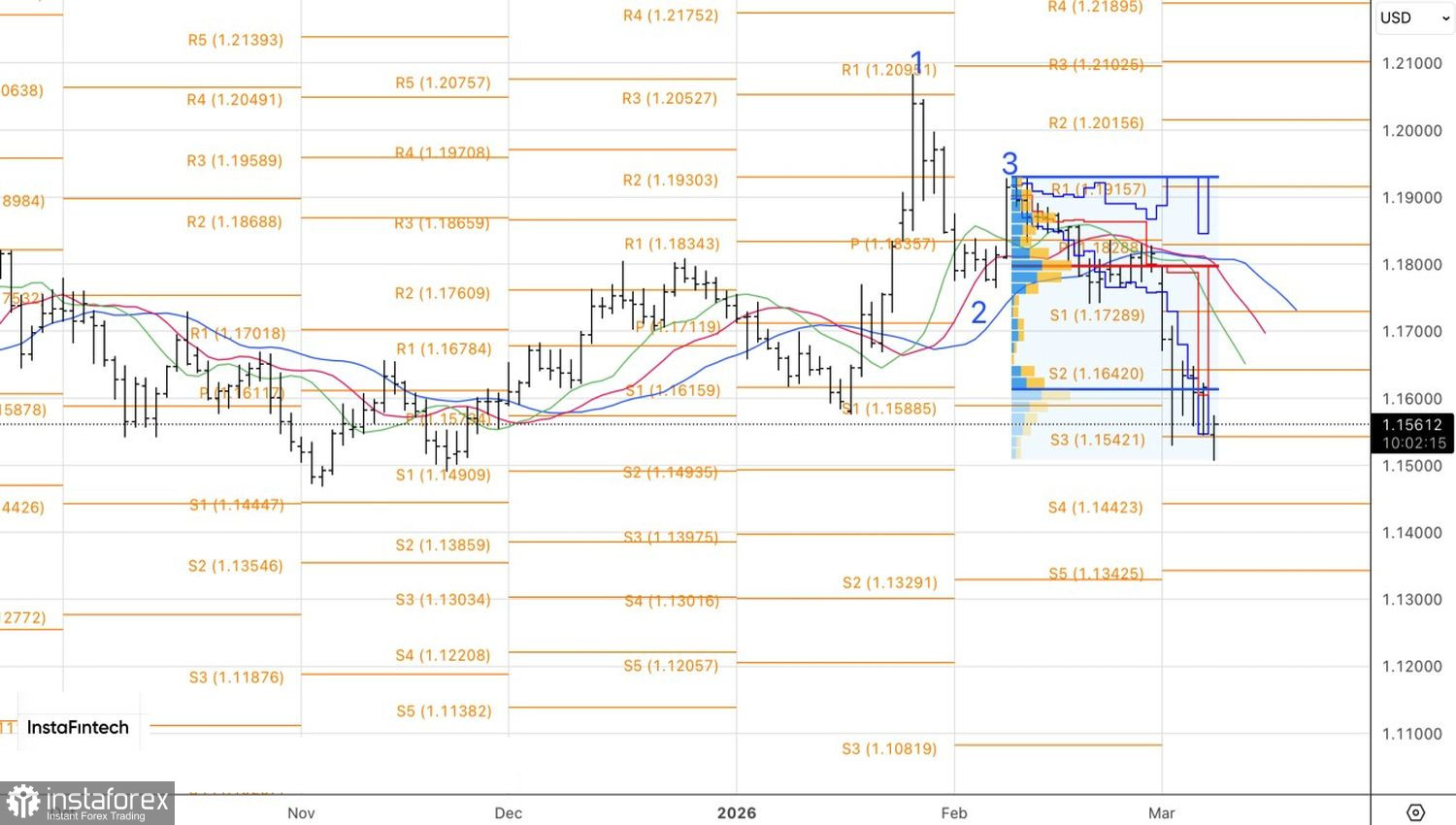

From a technical standpoint, on the daily chart, EUR/USD continues to decline due to the implementation of the 1-2-3 pattern. However, if a pin bar is formed, one could consider short-term longs above 1.1575. If the euro falls below $1.1540, it makes sense to continue selling.