See also

17.07.2026 12:47 AM

17.07.2026 12:47 AMBetter a thin peace than a good quarrel. It seems that Japanese authorities have realized this and, instead of another battle with the market by selling U.S. dollars, have decided to take a different approach — calling for domestic money to come home.

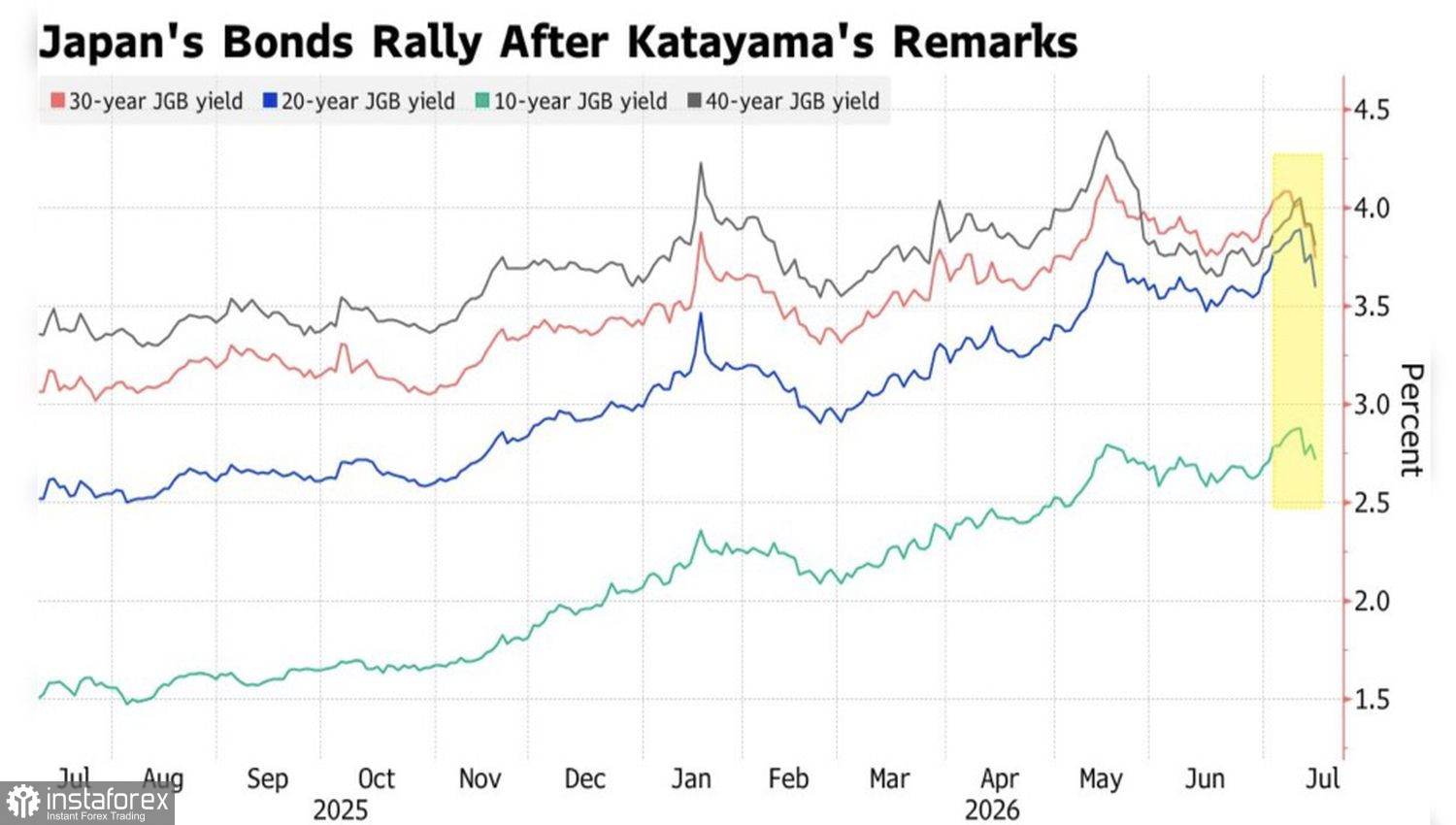

At the end of June, the yen reached a 40-year low against the U.S. dollar, which is no longer a one-off episode but the logical result of the combination of the Bank of Japan's ultra-low rates and Prime Minister Sanae Takichi's expansionary fiscal policy. Currency interventions at the end of April cost the treasury nearly $74 billion, but the effect proved fleeting. Traders comfortably price in a move for USD/JPY to 165 — which is about 1.6% above current levels. Investors, ironically, note that Tokyo promises to act "if necessary" each time but often limits itself to words.

This time, Finance Minister Satsuki Katayama decided to act not with words but with a different kind of deed. She urged large pension funds, including the giant GPIF with $1.8 trillion in assets, to increase investments in domestic assets. According to Societe Generale, the fund has room to buy up to £12.3 trillion ($76 billion) in Japanese government bonds without changing its portfolio structure. The market reacted with a rise in the yen and JGBs.

However, it's too early for USD/JPY bears to celebrate victory. Investors generally agree that redirecting capital back home can create a long-term source of demand for bonds and currency. Nevertheless, in the short term, markets are much more concerned with the interest rate differential and the ongoing carry trade — a strategy in which capital is borrowed cheaply in yen to invest in higher-yielding assets abroad. Each of these sales increases the supply of yen in the market and drives down its exchange rate.

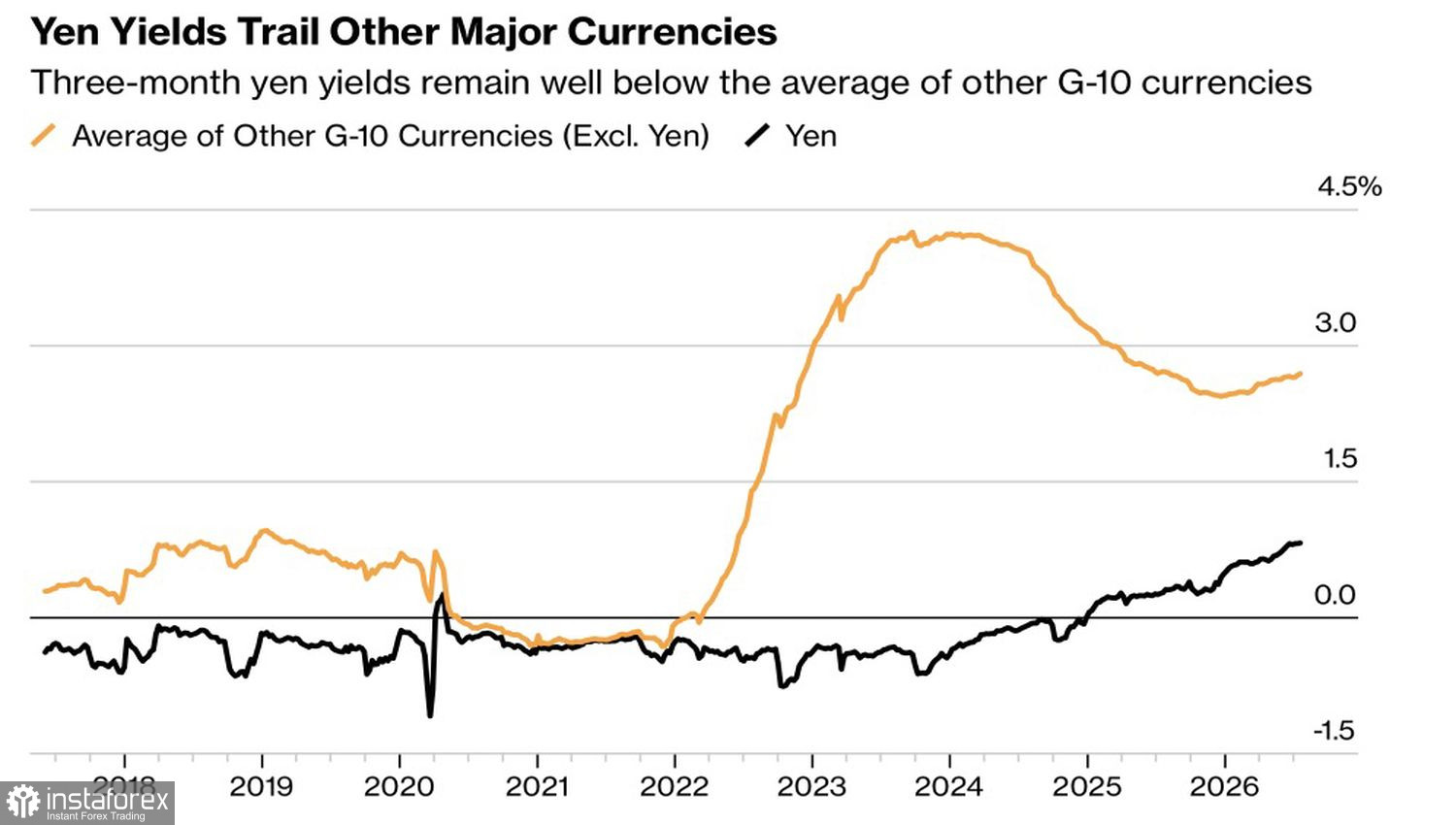

The BoJ is gradually raising rates starting in 2024 as it normalizes its policy. However, a base rate of 1% looks pale in comparison to 4.35% in Australia and a range of 3.50-3.75% in the U.S. — the gap is too great for speculators to voluntarily give up the yen as a funding currency.

Katayama emphasizes that the Ministry of Finance cannot dictate investment decisions to GPIF; changes will have to wait for significant progress in Japan's growth strategy. In my view, the idea is good on paper, but as long as the BoJ takes gradual action and Tokyo continues to increase budget expenditures, carry traders are unlikely to give up their usual pursuit of yield.

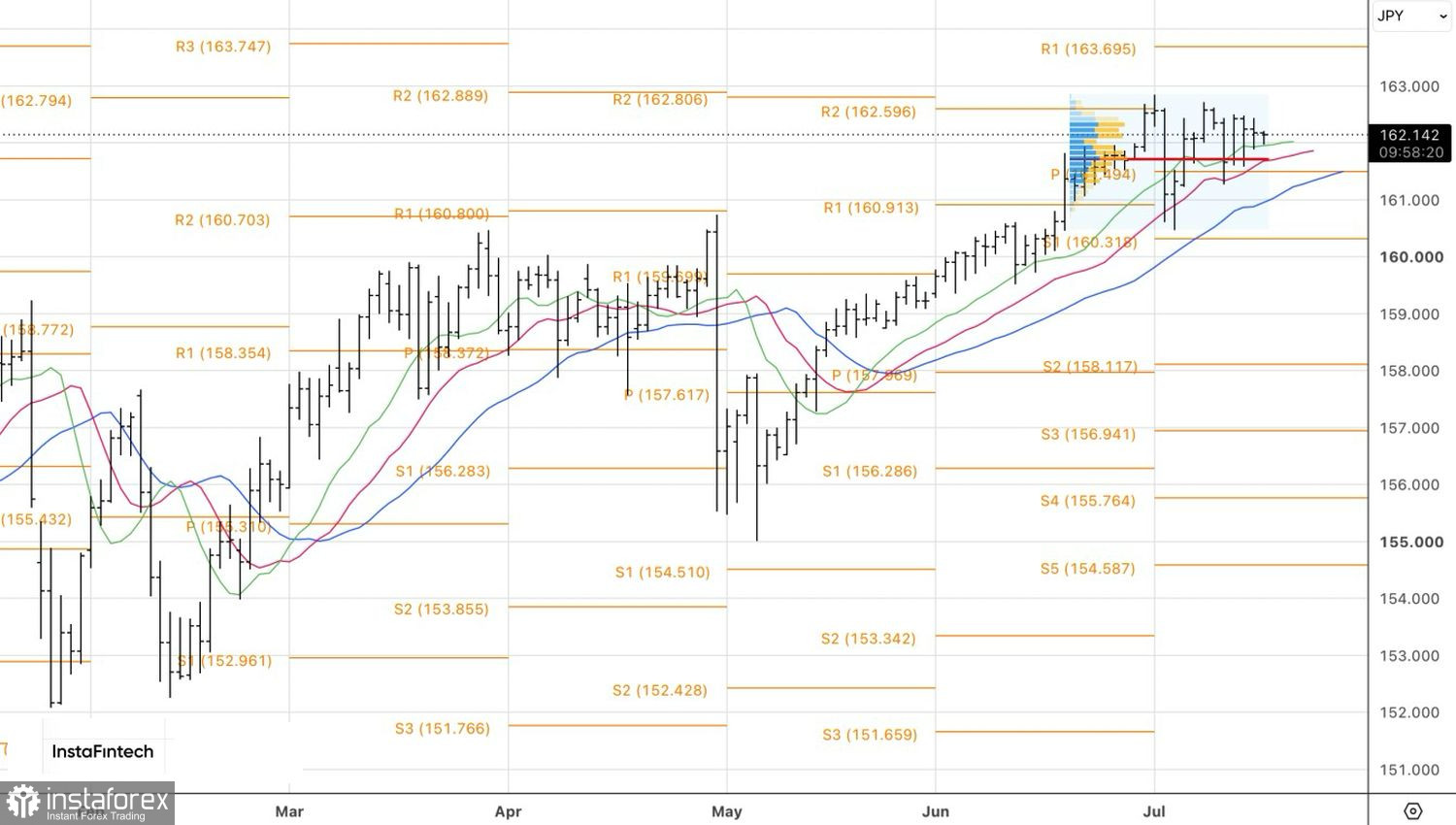

Technically, on the daily chart, USD/JPY is in short-term consolidation within the 161.60–162.50 range. A breakthrough of the lower boundary will provide grounds for opening short positions, while the upper boundary will support long positions. A more aggressive strategy involves playing the inside bar by placing two pending orders: from 162.40 to buy and from 161.85 to sell.