See also

17.07.2026 07:15 PM

17.07.2026 07:15 PM

The GBP/USD pair has posted strong gains in recent weeks, which may mark the beginning of a new bullish trend. This week, the bears proved unable to capitalize on developments, even though the Middle East experienced two additional escalations and negotiations once again reached a deadlock.

Donald Trump has already revoked Iran's authorization to export oil under the peace agreement and reinstated restrictions on Iranian ports. Meanwhile, Iran has once again closed the Strait of Hormuz from its side. The United States has now been conducting strikes against Iran for nearly a week, while Donald Trump continues to announce additional military action. As we can see, there is no real ceasefire in place.

For now, traders do not believe the conflict will escalate into a full-scale war, as similar situations have occurred several times before. In reality, however, hostilities have already resumed. Nevertheless, the geopolitical factor was largely priced in between February and May. Therefore, only exceptionally significant developments in the Middle East are likely to encourage investors to buy the US dollar again based on its safe-haven status.

This week, bullish traders received an unexpected boost as US inflation slowed to 3.5%. Shortly afterward, Kevin Warsh refrained from promising further monetary tightening during his testimony before Congress, triggering another wave of disappointment among dollar bulls. As a result, there is no longer any certainty that the Federal Reserve will begin tightening monetary policy as early as September.

Moreover, by September, the market should have a much clearer picture of the conflict in the Middle East, autumn oil and natural gas prices ahead of winter, and how inflation responds to the evolving energy and geopolitical environment.

Initially, the market expected US inflation to continue rising unless the FOMC intervened. Later, concerns about further price increases eased as oil prices declined to around $70 per barrel. This week, however, oil climbed to the $85–87 range, while the renewed escalation in the Middle East and the blockade of the Strait of Hormuz could push prices even higher.

If events develop according to the most pessimistic scenario, oil could return to the $100–120 per barrel range. Under such circumstances, any meaningful slowdown in inflation in either the United States or the eurozone would become highly unlikely. Conversely, if the situation develops according to a more optimistic scenario, oil prices could fall back to the $60–70 range, reducing the need for further monetary tightening.

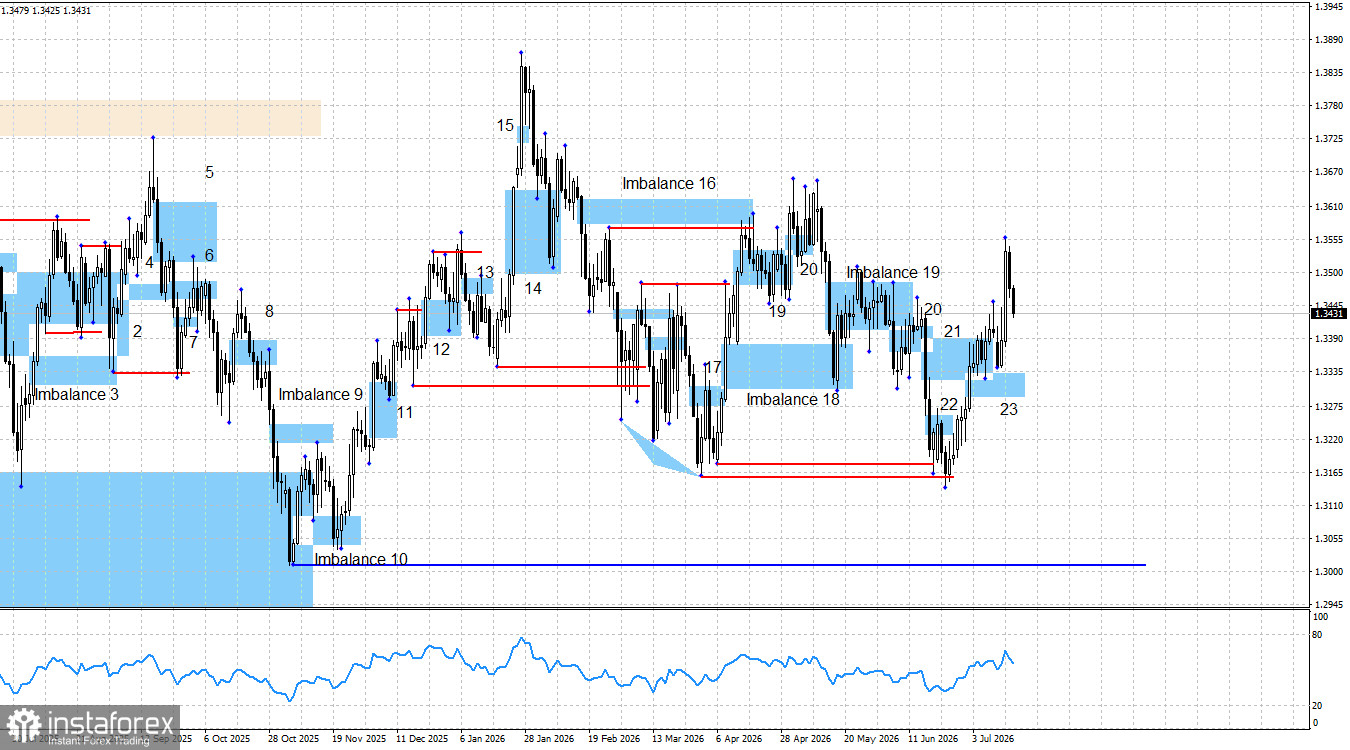

Technical analysis indicates that the bulls remain in control and may continue their advance. Price first swept liquidity below the April 6 low and then below the March 31 low. Therefore, there were solid technical reasons to expect further strength in the pound over recent weeks.

Given that the US dollar still lacks compelling long-term bullish drivers, despite its impressive gains during 2026, I believe the bears are unlikely to regain control. In addition, Bullish Imbalance 23 formed last week, and price reacted to it twice, providing traders with opportunities to open long positions. Bearish Imbalance 21 has now been invalidated.

Therefore, I expect either a continuation of the pound's advance or a resumption of the uptrend following the corrective pullback observed over the past two trading sessions. I would also note that a new bullish imbalance formed on Thursday. However, it is relatively small, so I have not yet marked it on the chart. Even so, there is a price gap in the 1.3440–1.3460 level that could still attract market attention.

Friday's economic calendar was relatively quiet. No significant data were released in the United Kingdom, while several US reports had little impact on market sentiment. This week's trading was dominated by inflation data, which substantially weakened the outlook for the US dollar.

Overall, the broader fundamental backdrop still leads me to expect further long-term weakness in the US dollar. Neither the conflict between Iran and the United States nor the possibility of Federal Reserve rate hikes in 2026 has materially altered that outlook.

Geopolitical tensions temporarily reminded the market of the dollar's safe-haven appeal, but the conflict has already moved beyond its most active phase. Although the Federal Reserve intends to raise interest rates during 2026, which is supportive for the dollar, tighter monetary policy would also slow economic growth and weaken the labor market.

It should also be remembered that Kevin Warsh was appointed by Donald Trump to lead the FOMC specifically because he was expected to pursue a more accommodative monetary policy than Jerome Powell. Consequently, in my opinion, any appreciation of the US dollar should be viewed as temporary rather than the beginning of a sustainable long-term trend.

The economic calendar for July 20 contains no significant scheduled releases. Therefore, macroeconomic data are not expected to influence market sentiment on Monday.

The long-term outlook for the pound remains bullish. Following liquidity sweeps below the two most recent swing lows, bulls regained control of the market.

The pound could still resume its decline toward 1.3007, the level that would invalidate the broader bullish trend, but such a move would require fresh bearish technical signals. Since Bearish Imbalance 21 has already been invalidated, no such signal is currently present.

The bullish case is supported by two liquidity sweeps as well as Bullish Imbalance 23. Price has already reacted to Imbalance 23, while the next upside targets are the highs of May 1 (1.3656) and January 27 (1.3867).

A new Bullish Imbalance also formed yesterday following Wednesday's strong rally in the pound.