Veja também

02.04.2026 12:35 AM

02.04.2026 12:35 AMThe war in the Middle East, as expected, has negatively impacted consumer confidence, leading to a sharp rise in inflation expectations (up to 5.7% from 4.7% in February) and concerns about overall economic prospects. ANZ Bank has lowered its forecasts for the labor market and housing prices, with the labor market recovery postponed by a couple of quarters. Real wage growth in the private sector is expected to turn negative.

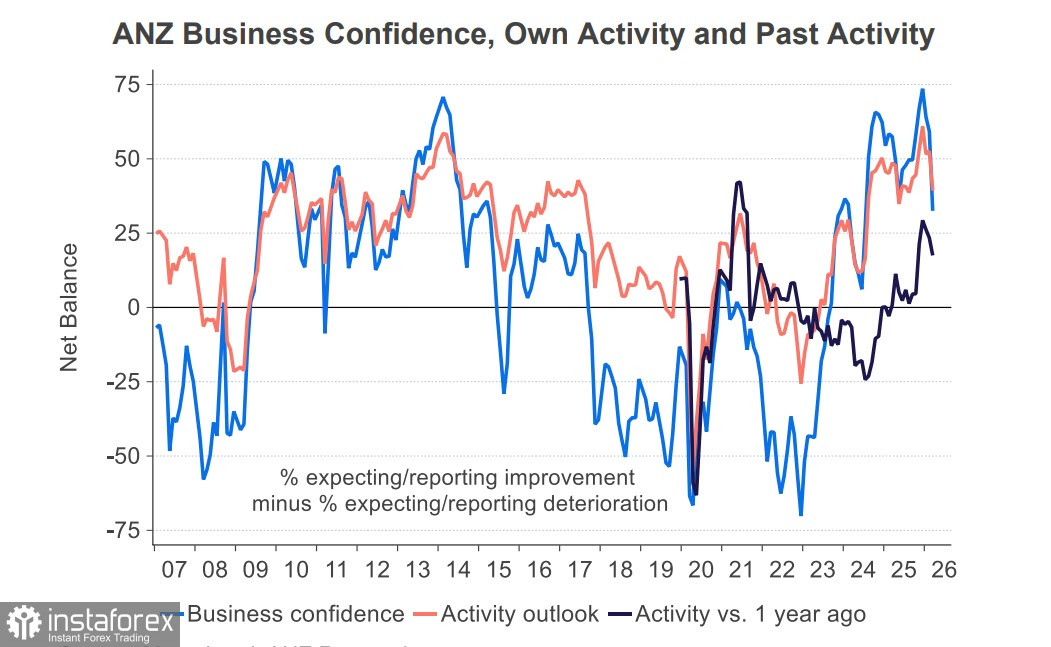

The business confidence index dropped by 26 points in March, from 59 to 33—this is also a result of the oil shock. The percentage of firms expecting price increases over the next three months rose by 7 points to 60%. The net percentage of firms expecting increased costs (85%, compared to 79%) is the highest since the beginning of 2023.

The government is already reacting to the shock—with a support package for rising living costs announced last week, providing a temporary payment of $50 per week to low-income working families. It is unnecessary to remind that this is yet another step toward higher inflation.

The Reserve Bank of New Zealand (RBNZ) will hold its next meeting on April 8. Bank Chief Adrian Orr has already outlined his views in a keynote speech titled "Global Disruptions on New Zealand's Shores: The Impact of the Iran Conflict on New Zealand." He perceives a jump in prices (and who doesn't?), but rates will only change if the consequences are persistent. For now, of course, that is not the case, meaning no rate change will occur at the upcoming meeting.

Key data this week is coming from the US. The private sector employment report showed growth above expectations, as did the ISM Manufacturing Index, with growth driven by a sharp increase in the price index, while employment and new orders performed worse than in February. The current surge in enthusiasm, which led to falling oil prices and a declining dollar index, can be considered a temporary phenomenon, as it is based solely on rumors and has not been supported by any real evidence.

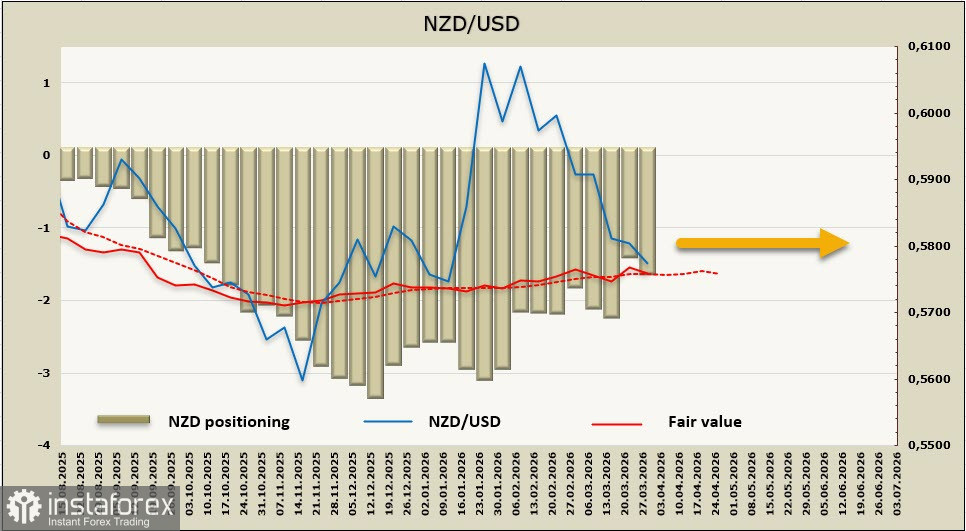

The net short position on the NZD increased by $0.2 billion over the reporting week to -$1.57 billion, with positioning remaining bearish and the calculated price lacking direction.

Last week, we suggested that if the conflict in the Gulf escalates, the kiwi would continue to decline towards 1.5533. This scenario has become more likely as negativity was intensified by weak New Zealand GDP data for the fourth quarter. The downward movement continues to look preferable, as the attempt at a rebound is based solely on Trump's verbal interventions about the possibility of an imminent end to the war, which lack real facts, meaning the enthusiasm rests on too shaky a foundation. We see resistance at 1.5780/5800, above which growth is possible only with an increase in optimism.