Vea también

01.05.2026 12:55 AM

01.05.2026 12:55 AM

During his speech, Jerome Powell also acknowledged that interest rates might be lowered in the coming months, but such a scenario now seems like a utopia. Most likely, Powell tried to smooth things over after three Federal Reserve governors demanded the removal of the phrase about potential monetary policy easing from the final communique. As usual, Stephen Moore voted in favor of an immediate rate cut.

Powell also mentioned that he will remain on the FOMC for an indefinite period. It seems that Powell wants to become a "controlling figure" within the central bank. He noted that in recent years, legal attacks from the president's administration have increased, and these attacks are undermining the institution and threatening public values. As a result, Trump will not be able to appoint a new FOMC member to replace Powell. This means one less "dovish" vote at each central bank meeting. Powell stated that he will leave the Fed when he deems it necessary. At this time, he is waiting for the investigation against him to be fully and definitively concluded.

From all of the above, one conclusion remains clear: how will the new Fed president maintain "dovish" views amid rising inflation? Certainly, if the Strait of Hormuz is unblocked in a few months and inflation begins to move toward 2% rather than away from it, a return to rate-cutting policy by the Fed would be appropriate. However, Warsh will likely demand easing from day one. And what if the blockade of the Strait of Hormuz continues throughout 2026?

No matter how much the dollar wants to gain, it has not benefited from the Fed's slightly more "hawkish" stance than earlier. The situation with the Fed is currently as tangled as that between Iran and the U.S., as well as the situation with the Strait of Hormuz. Market participants reasonably concluded that conclusions should be drawn not from Powell's last meeting but from Warsh's first meeting. In my view, if bombings of Iran do not resume, the demand for the U.S. currency will continue to slowly decrease. In this case, the wave patterns of the EUR/USD and GBP/USD instruments will take on a slightly different form, and the construction of upward trend segments may resume. Given these circumstances, I cannot currently envision what, aside from geopolitics, could drive the market to actively increase demand for the U.S. currency again.

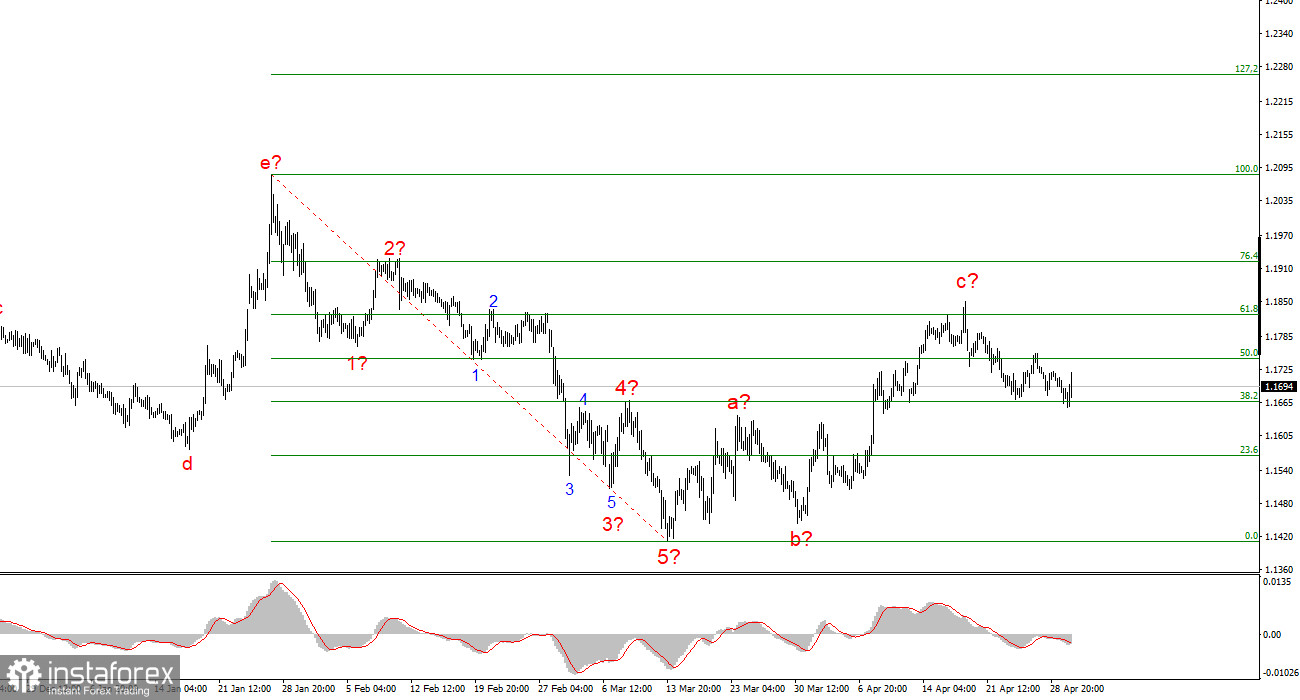

Based on the analysis of EUR/USD, I conclude that the instrument remains within an upward section of the trend (bottom picture) and, in the short term, is within a corrective structure. The corrective wave set appears to be complete and may take on a more complex, extended form only if the geopolitical background in the Middle East improves. Otherwise, from current positions, a new downward wave set may begin to form. We have observed the corrective wave; further developments will depend on market belief in a favorable outcome of negotiations.

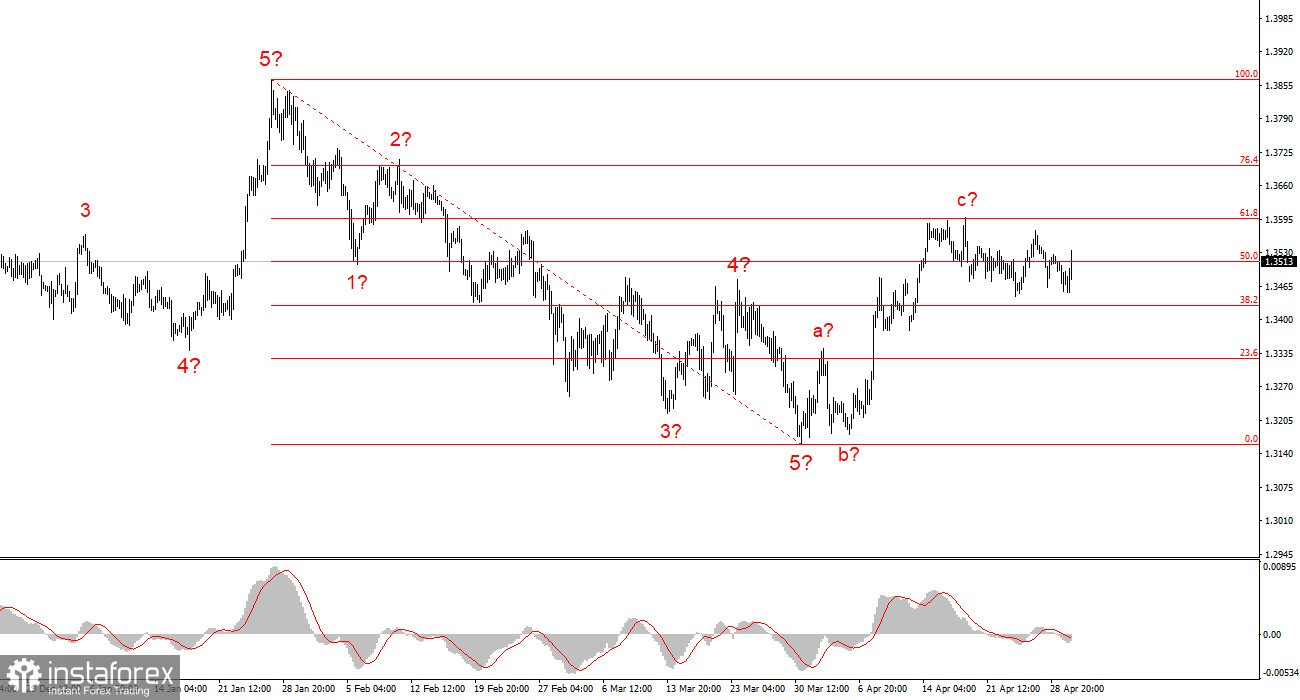

The wave pattern for GBP/USD has, over time, become clearer, as I anticipated. Now we see a clear three-wave upward structure on the charts, which may already be complete. If this is indeed the case, we can expect the formation of at least one downward wave (presumably d). The upward segment of the trend could take on a five-wave form, but for that to happen, the conflict in the Middle East must subside rather than reignite. Therefore, the baseline scenario for the coming days is a decline towards the 34 figure or slightly lower. Again, everything will depend on geopolitical factors.