Vea también

25.02.2026 12:47 AM

25.02.2026 12:47 AM

Despite the rather mediocre results of Trump's trade policy, economists note that in the last month of the previous year, the trade balance deficit was $70 billion, resulting in a cumulative deficit of $900 billion for the entire year of 2025. In December, imports increased while exports declined. Thus, we again see the picture we've observed for years: weak exports and strong imports.

Economists also took the time to review statistical data from the last 60 years. It turned out that the trade balance deficit in 2025 was nearly a record high over the last six decades, totaling $900 billion, with only 2022 and 2024 recording larger deficits.

Based on all the above, I can say that the results of Trump's trade policy are unsatisfactory. Global issues in the U.S. economy were not eradicated, and many economists question whether it was worth attempting to eradicate them at such a cost. I repeat: America has lived with rising national debt, a budget deficit, and a trade deficit for decades. This model has always worked. Moreover, almost all countries worldwide have some form of national debt, and many have a negative trade balance. The problem lies not in the effectiveness of governance and trade policy but in the very nature of the economy itself. If the economy is export-oriented, the trade balance will very likely be surplus. For example, the European Union recorded a minimal deficit only once throughout the entire year of 2025. If the economy is import-oriented, it is evident that the country buys more than it sells.

In my opinion, Trump's trade policy will not yield significant results. The national debt will continue to grow, and if all tariff collections from 2025 have to be returned, it would deal a severe blow to the budget and the economy. Furthermore, it is unclear what tariff rates will apply in the long term following the Supreme Court's decision. Currently, Trump has set a uniform 15% rate for all countries. However, the president cannot impose a higher tariff, nor can he set different tariff rates for different countries. After 150 days, the U.S. Congress must approve the extension of these tariffs if Trump wishes to keep them. Therefore, the level of uncertainty regarding tariffs in February 2026 has increased even more.

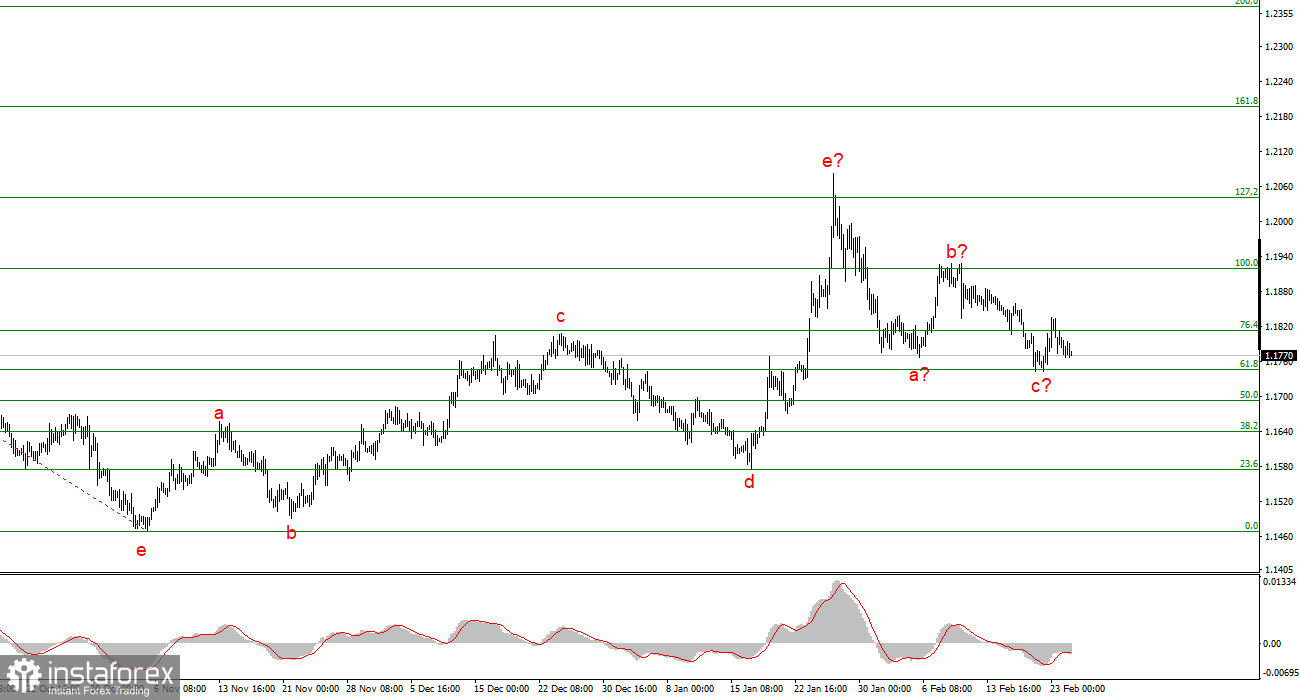

Based on the analysis of EUR/USD, I conclude that the instrument continues to build an upward trend segment. Trump's policies and the Federal Reserve's monetary policy remain significant factors contributing to the long-term decline of the American currency. The targets for the current segment of the trend may extend up to the 25th figure. At this moment, I believe that the instrument remains within the framework of global wave 5, so I expect an increase in quotes in the first half of 2026. The corrective structure a-b-c could end at any time, as it has already taken a convincing form. I believe it is now advisable to search for areas and levels for new purchases with targets located around 1.2195 and 1.2367, corresponding to 161.8% and 200.0% on the Fibonacci.

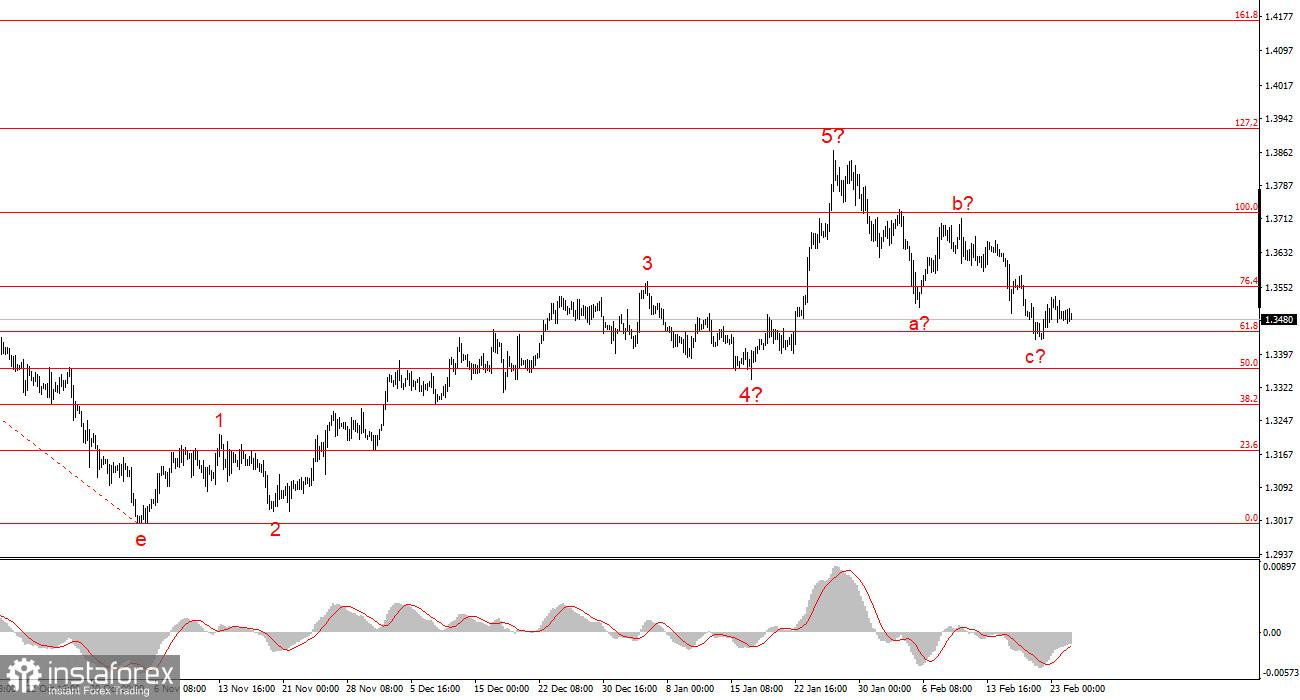

The wave analysis of the GBP/USD instrument appears quite clear. The five-wave upward structure has completed its formation, but global wave 5 may take a much more extended form. I believe that the construction of a corrective wave set may soon conclude, after which the upward trend will resume. Therefore, I can now advise seeking opportunities for new purchases with targets positioned above the 39 figure. In my opinion, under Trump, the British pound has a good chance of rising to $1.45-$1.50.