Vea también

26.05.2026 02:12 PM

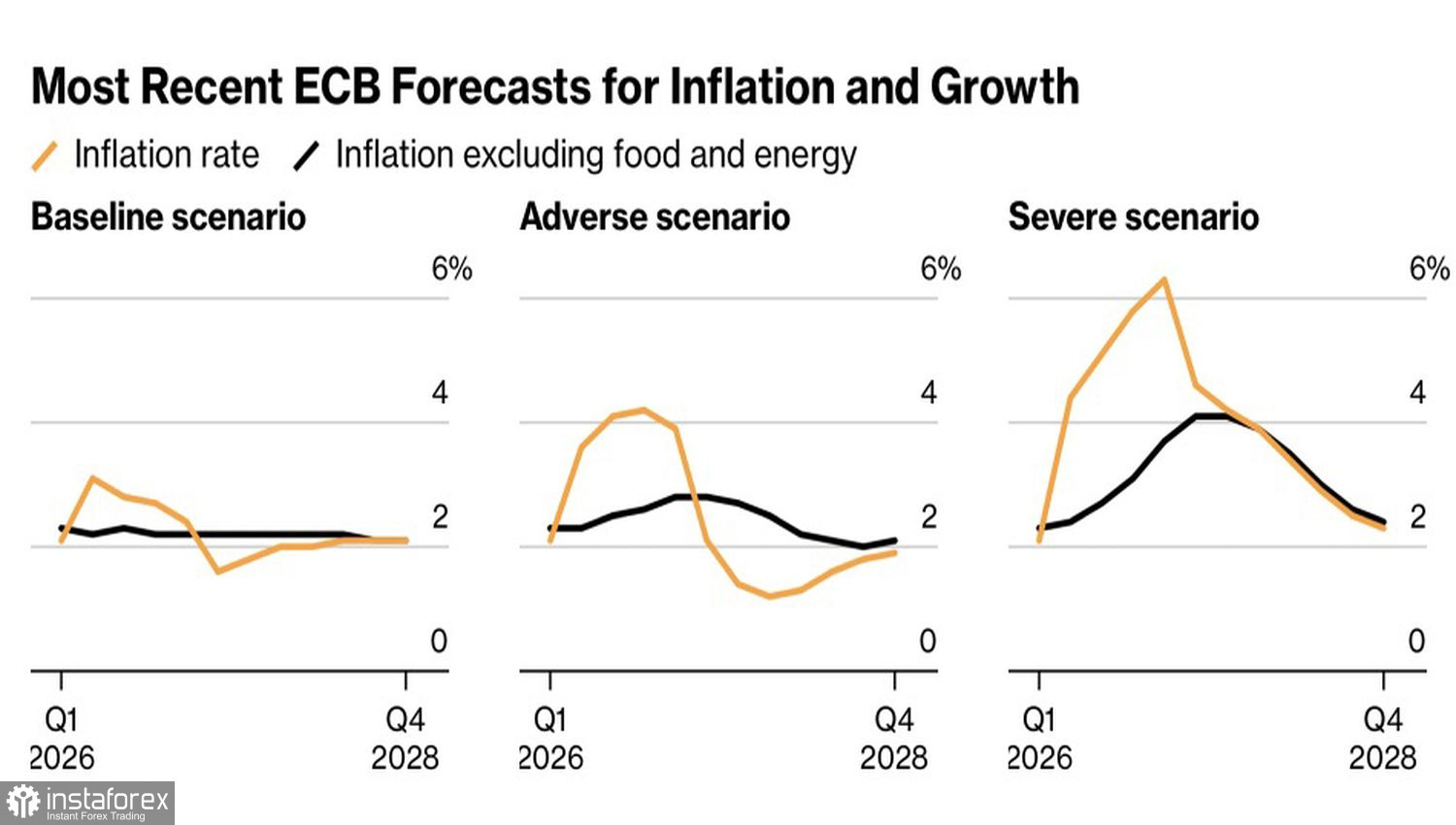

26.05.2026 02:12 PMEven if the armed conflict in the Middle East ended tomorrow, central banks would still need to raise interest rates. The energy infrastructure of Persian Gulf countries has suffered significant damage; until the region is rebuilt, oil prices will remain higher than before the bombing started. That means higher inflation in the eurozone and a need for the ECB to fight it — so said ECB Governing Council member Isabel Schnabel. EUR/USD bulls are already using her remarks to prepare for an attack.

ECB inflation outlook for Europe

The US dollar still cannot decide on a direction because contradictory information keeps coming from the Middle East. At times, the White House speaks of progress in talks with Iran and expresses confidence in a deal; at other times, explosions rock the region again. After an attack on mine?countermeasure vessels, Tehran began bombing US bases; the United States replied symmetrically. But can this be considered a violation of the ceasefire that amounts to an escalation?

Neither the US nor Iran seem to think so. Both continue dialogue on a peaceful settlement, although they occasionally make loud, aggressive statements. Donald Trump insists he will either secure a good deal or there will be no deal at all — and if there is no deal, new bombings that are worse than before will begin. Supreme Leader Mojtaba Khamenei says the countries of the Middle East will no longer serve as shields for American bases.

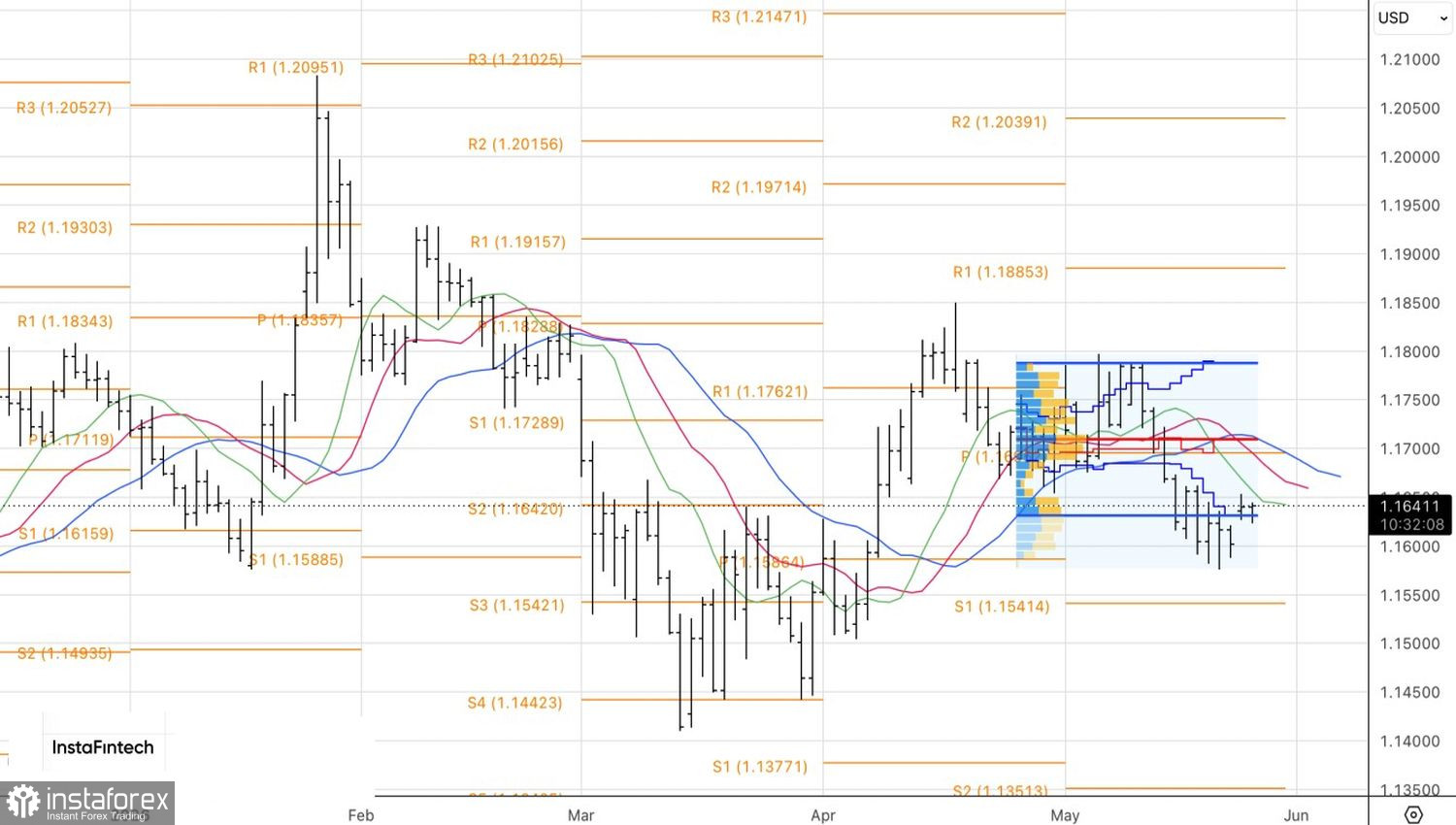

The futures market reacts to Washington and Tehran's rhetoric with a pinch of salt. Derivatives currently price about a 55% chance of a Fed funds rate hike in 2026. The flattening of the yield curve signals that the Federal Reserve may have no choice but to tighten monetary policy.

US yield-curve dynamics

Credit Agricole believes investors need not worry about the fate of the USD index. Its dynamics are still governed by the "dollar smile" theory. If the US currency fails to benefit from recession fears stemming from the Middle East conflict and a closure of the Strait of Hormuz, it will have another trump card: a rise in global risk appetite.

Despite a quite likely ECB rate increase on deposit facilities in June, borrowing?cost differentials will remain skewed in favor of the US dollar. That will allow carry traders to use the greenback as a funding currency amid equity rallies and declining FX volatility.

Technically, the daily chart of EUR/USD still shows a battle at the lower band of the fair?value range of 1.163–1.1785. A victory for the bulls would increase the chances of a continued rally and be a trigger to buy euros. Conversely, their defeat would reopen the strategy of selling the major currency pair.