Lihat juga

28.05.2026 12:41 AM

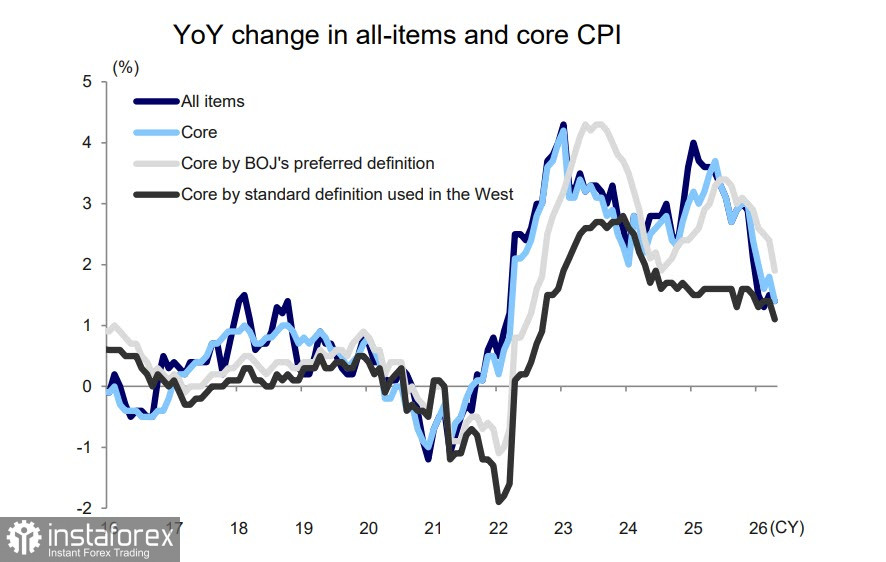

28.05.2026 12:41 AMIn April, consumer inflation in Japan declined. The core consumer price index (CPI) slowed from 1.5% to 1.4% year-on-year, while the core index excluding fresh food also decreased from 1.8% to 1.4%. An even more significant slowdown was observed in the second core measure that the Bank of Japan (BoJ) uses to assess inflationary pressure, which excludes both food and energy: it fell from 2.4% to 1.9% year-on-year.

Despite government measures such as subsidizing gasoline prices and waiving school meal fees, it is evident that food inflation is also declining steadily. This suggests that the current geopolitical tensions in the Middle East, including the situation surrounding the Strait of Hormuz, are having a limited impact on Japanese inflation. This is particularly noteworthy considering that Japan imports the overwhelming majority of its oil from the Persian Gulf.

Analysts at Mizuho predict that the impact of rising oil prices will not become evident until at least July. However, this forecast is not definitive, as the government plans to resume subsidizing household electricity and gas bills during the summer peak consumption period.

At present, there is no observed necessity for the BoJ to raise interest rates, except for the factor of a weakening yen. The yen is expected to continue weakening if the BoJ again pauses its monetary policy. However, a rate increase aligns with the United States' interests.

On May 20, Reuters reported that shortly after a meeting between U.S. Treasury Secretary Bessent and Japanese Prime Minister Takaichi on May 12, government officials received information that he had "directly requested Takaichi to raise rates" (though the details of the discussions are kept strictly confidential). If the U.S. government indeed exerts pressure on Takaichi's administration, the chances of a rate increase in June are rising, making this the most likely scenario for the market.

BoJ Governor Ueda refrained from commenting on the specifics of his discussions with Yellen but acknowledged that the war in the Middle East contributes to rising prices. Analysts at Mizuho lean toward the idea that inflation will resume its upward trend in the second half of the year and will be significantly above the BoJ's target. It is likely that the BoJ will raise rates in June to alleviate pressure on the yen, which has long been at too low a level.

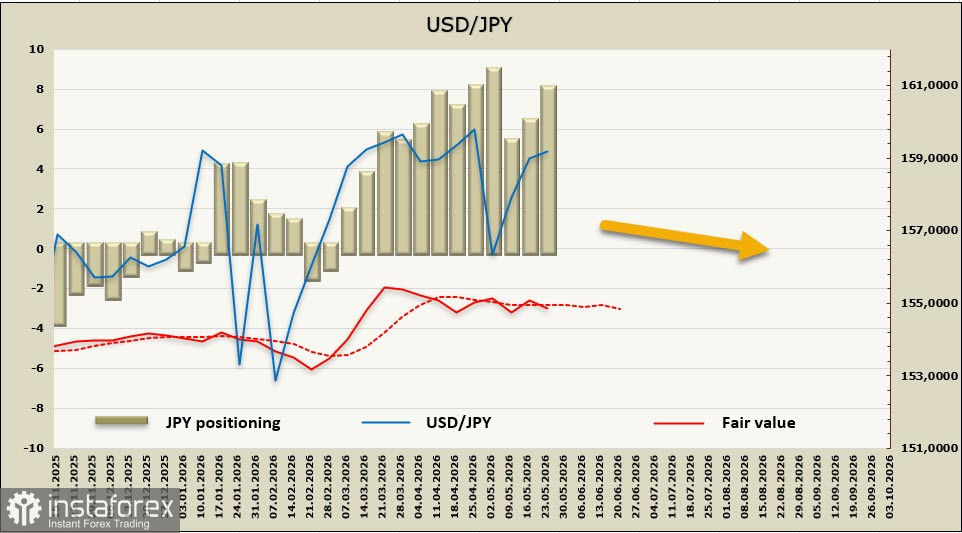

Speculative positioning on the yen is bearish, but the calculated price still lacks momentum. Factors capable of directing the yen are mutually blocking each other. Market factors are pushing USD/JPY higher, with neither promises of rate hikes nor rising yields on Japanese bonds providing support. The yen has hit another low since the last currency intervention on April 30, and players will again have to choose between fear and greed. Fundamentally, selling the yen appears justified and potentially profitable; however, the BoJ may conduct a large-scale intervention at any moment, and this threat is likely to prevent the USD/JPY pair from approaching the resistance level of 162.