Vea también

19.05.2026 02:43 PM

19.05.2026 02:43 PMThe pound opened the week with a modest corrective gain after political tensions in the United Kingdom eased following the Conservatives' unexpected election setback and after the US president announced he would not strike Iran on May 19, a development that reduced overall geopolitical risk.

The UK labor market report offered no major surprises, except that average wage growth rose rather than fell as expected, reviving concerns about broader inflationary pressures.

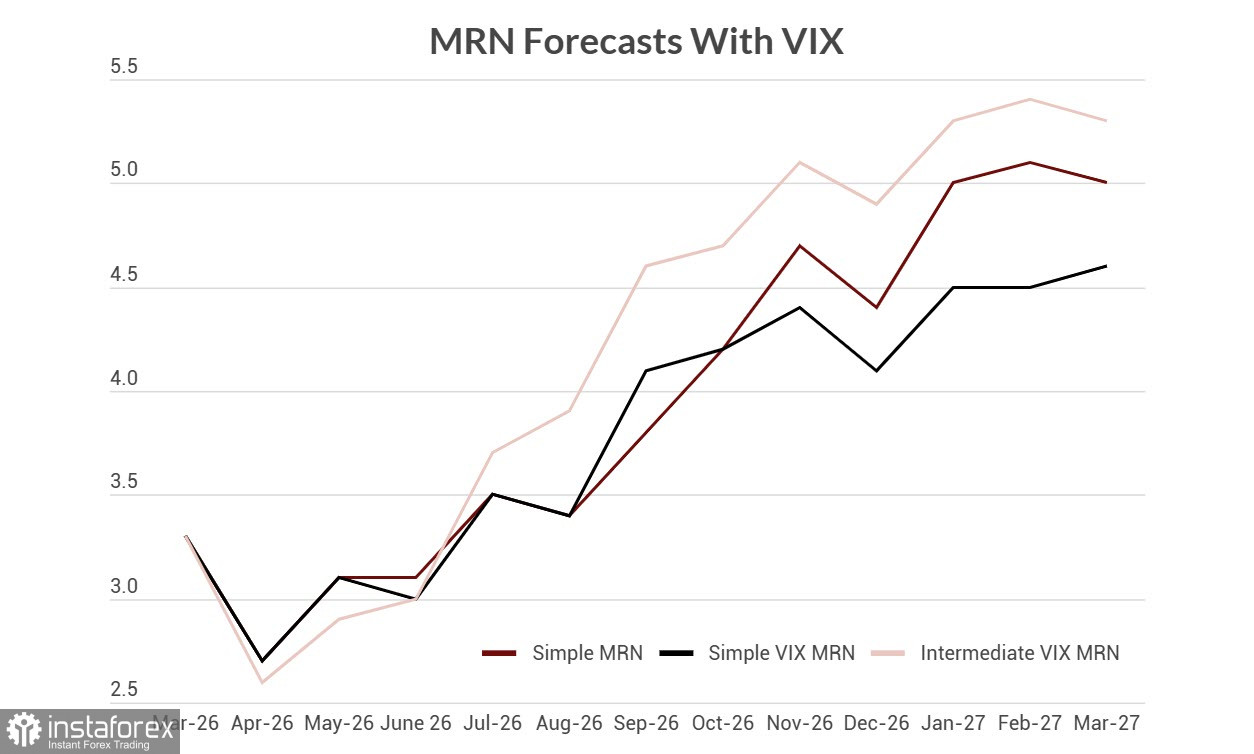

Inflation now looks highly unpredictable. Prior to the attack on Iran, forecasts suggested inflation in April could fall to around 2% or lower; it is now clear that inflation will increase, potentially significantly. The Bank of England expects inflation of about 3.1% in Q2 2026 and 3.3% in Q3 2026, with a peak of 6% by year-end if the conflict is prolonged. The National Institute of Economic and Social Research (NIESR), using a multi-recurrent neural network (MRN) model, projects inflation to rise through March 2027, although its peak is slightly lower than the Bank of England's forecast.

The outlook for the UK economy hinges on the balance between rising inflation and slowing growth. Revised GDP data for Q1 surprised on the upside, showing growth of 2.6% year-on-year versus a preliminary estimate of 1%. Until recently, markets expected the Bank of England to deliver two further hikes this year, and possibly three under certain conditions. Strong economic momentum, supported by high PMI readings in April and May, gives the Bank scope to pursue a more aggressive tightening path if inflation continues to rise.

April inflation data is due on May 20. Consensus short-term forecasts for April are moderate and even below March readings. The pound's reaction to the release could be mixed:

- If inflation exceeds expectations, the probability of additional rate hikes will rise materially, likely prompting a significant sterling appreciation.

- If inflation is in line with or slightly below forecasts, markets are unlikely to react strongly.

A growth slowdown now appears almost inevitable. The IMF in April lowered its 2026 UK GDP forecast from 1.3% to 0.8%, citing gas import dependency and expectations of a less aggressive Bank of England. Accordingly, if April inflation accelerates, the Bank of England would have scope to raise rates as soon as June, rather than waiting for clear evidence of slowing activity; markets may interpret that possibility as bullish for sterling.

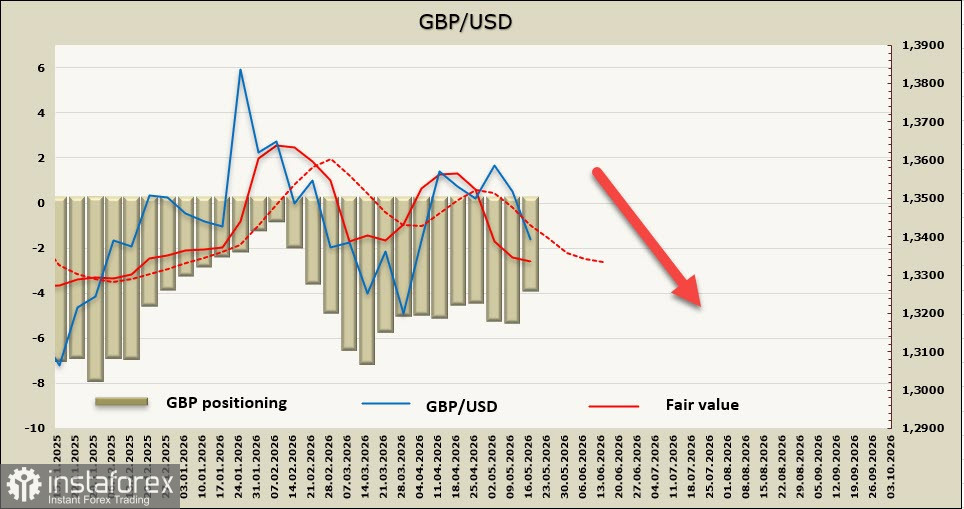

Net short positions on sterling narrowed by GBP 1.8 billion over the reporting week to -GBP 3.8 billion, but the implied price remains below the long-term average and is still biased toward further declines.

A week earlier the priority scenario was a decline in GBP/USD toward support at 1.3450–1.3470. The pound did plunge under pressure from escalation risk and failed to find support. The probability of a corrective rally is considered low; attempted rallies toward 1.3450–1.3470 are likely to prompt renewed selling. The revised downside target is the March low at 1.3157.