Vea también

08.07.2026 12:24 AM

08.07.2026 12:24 AMThe labor market data released on Thursday was weaker than expected, triggering a rise in U.S. and European government bond yields and a weakening of the dollar against the euro and the yen. The weak data reduced expectations for aggressive rate hikes by the Fed, which had previously been based on optimistic macroeconomic indicators.

Amid the data release, Donald Trump once again criticized the Federal Reserve 's policy. He suggested that Kevin Warsh is facing resistance from the central bank, which does not want to ease monetary policy. Trump reaffirmed his intention to push for the dismissal of Lisa Cook and Jerome Powell, whom he considers supporters of a "hawkish" stance.

Following the labor market report, forecasts regarding the Fed's rate were predictably adjusted. Markets now expect a rate hike in September, with the probability of a July hike reduced to 25%, and do not foresee any changes until the end of 2027. It goes without saying that such long-term forecasts have negligible value, aside from one aspect—there is too much uncertainty.

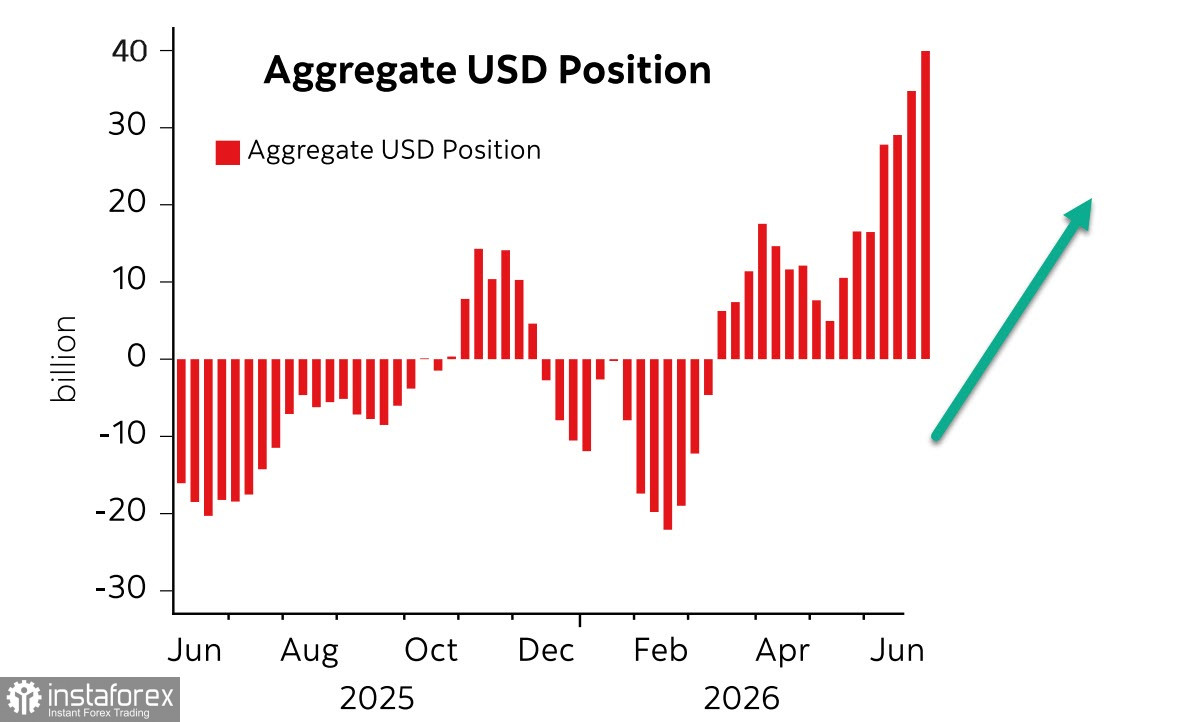

Meanwhile, the latest CFTC report showed that the U.S. dollar continues to dominate the futures market. The total long position against major world currencies increased by $5.4 billion over the reporting week, reaching $39.7 billion, the highest level since 2015.

This strong imbalance may signal a reversal, but there are currently no clear signs of one. Yes, the opening of the Strait of Hormuz and ongoing negotiations between the U.S. and Iran aimed at reaching a long-term agreement are clearly reducing geopolitical tensions, but the situation with energy supplies through the strait remains far from normal. Traffic has only resumed to a quarter of pre-war levels, and it will take several months to normalize both current supplies and reserves. During this time, the crisis could see new developments, at least in the food sector, due to a clear fertilizer shortage.

Moreover, the news from the U.S. is not particularly optimistic. After the weak labor market report, the RCM/TIPP Optimism Index was published. At first glance, there is an improvement, with the index rising to 45.5 in July from 42.5 in June, marking an increase of 3.0 points (7.1%). This is the sharpest monthly increase since November 2024, breaking a three-month period of stagnation near April's lows. However, the index has remained below the neutral mark of 50 for 11 consecutive months, indicating pessimism, and is 7.3% lower than the historical average over 306 months.

The U.S. trade balance deficit sharply increased to $77.6 billion in May, the highest level in over a year, returning to levels seen at the end of 2024. This outcome effectively nullifies the positive effect of increased tariffs and indicates a risk of GDP contraction in the second quarter.

Overall, the situation is far from positive. Rising trade and budget deficits, weakness in the labor market, reduced consumer activity, and simultaneous high stress levels combined with a high Fed rate and the prospect of further increases do not signal a reduction in tension. Therefore, the likelihood of further strengthening of the U.S. dollar as the primary safe-haven currency remains high.